| Taxation | Cap'n Trade | Command&Control |

|---|---|---|

| Cost effectiveness | ||

| Yes, under condition | Yes under conditions: | No, very different implicit prices |

| If applied to all, with same price | If applied to all (high t.c.) | Unless cost & transaction costs are low |

| No free allowances | ||

| Uncertainty of cost uncertainty of quantities | ||

| Superior in simple framework, as quantities are a stock | Inferior, but quantités are a stock and investment is also | Very (too?) flexible, |

| Price stability is key to long term decision | Second order depends on comparative slope of marginal cost and marginal benefit | Long term efficiency (through banning) |

| Central bank type monitoring of market can stabilze price and mimick tax | ||

| Governance | ||

| Tax legislation, in the hand of finance committee in parliament, not green usually | Specific legislation committees | Very specific legislation up to arbitrary and opaque decisions |

| Use of receipts symbolically important (not relevant however) | no unanimity needed in the EU | open to lobby influence, hard to commit in the long term |

| very flexible to changes in technology | ||

| International agreements | ||

| In the UE tax legislation requires unanimity | international agreement and linkage possible | National only except trhough norms applied to imported products |

| International binding agreements impossible due to principle fiscal sovereignty | Free allowances can induce carbon leakage (hard to compensate with BTA) | |

| BTA | ||

| Possibility of capture or fraud | ||

| Strong institutions for tax compliance | Market manipulation possible, but not likely to be an issue | Impossible to equilibrate pressure |

| Manipulation of outcomes | ||

| Principle of equal taxation | Frauds due to different juridictions and linkage | Monitoring costs and frauds high |

| Small number of units under trade scheme, caputure by lobbies likely (similar to interbank market) | ||

| Inter state compensation (hot air) | ||

| Information, monitoring and compensation | ||

| Low costs if taxation is upstream for CO2 emissions | Low for large units, nearly impossible for small ones – taxes and t&c must coexist | Very difficult to monitor |

| High if monitoring is downstream | International markets raise taxation cooperation issues and free rider with another policies interactions | Compensation at the cost of higher emissions (tradeoff between target and compensation) |

| Compensation is difficult (downstream, high information and monotoring cost) or compensation is lumpsum kind (average compensation, double dividend) | Upstream compensation very easy | |

| Heterogenity | ||

| One size fits all | Easily reveal social cost | Very suited to tailored policies, with efficiency loss unquantifiable |

| Potentially corrected with BTA, with loss of efficiency | Limit extreme pressure on high polluters | |

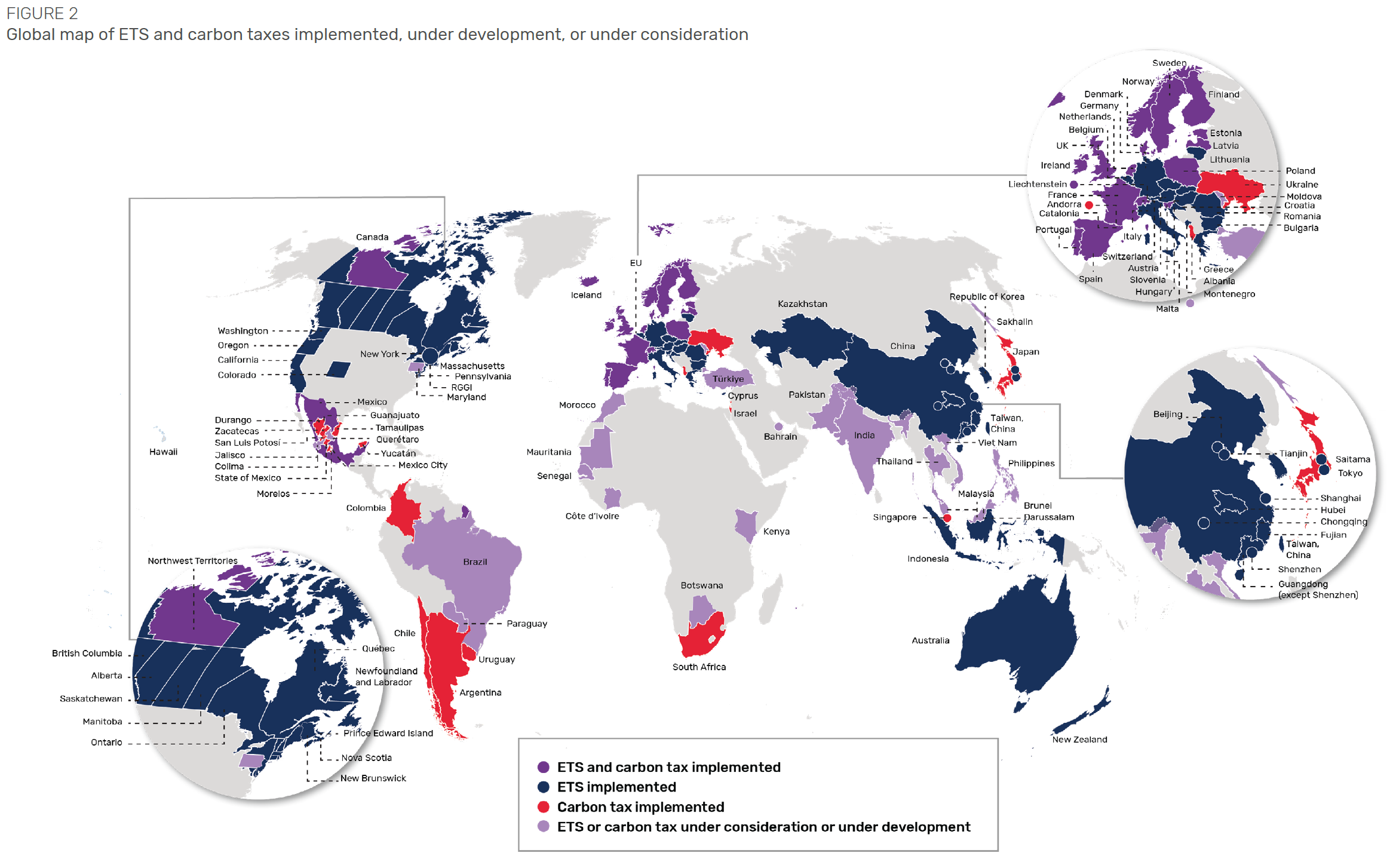

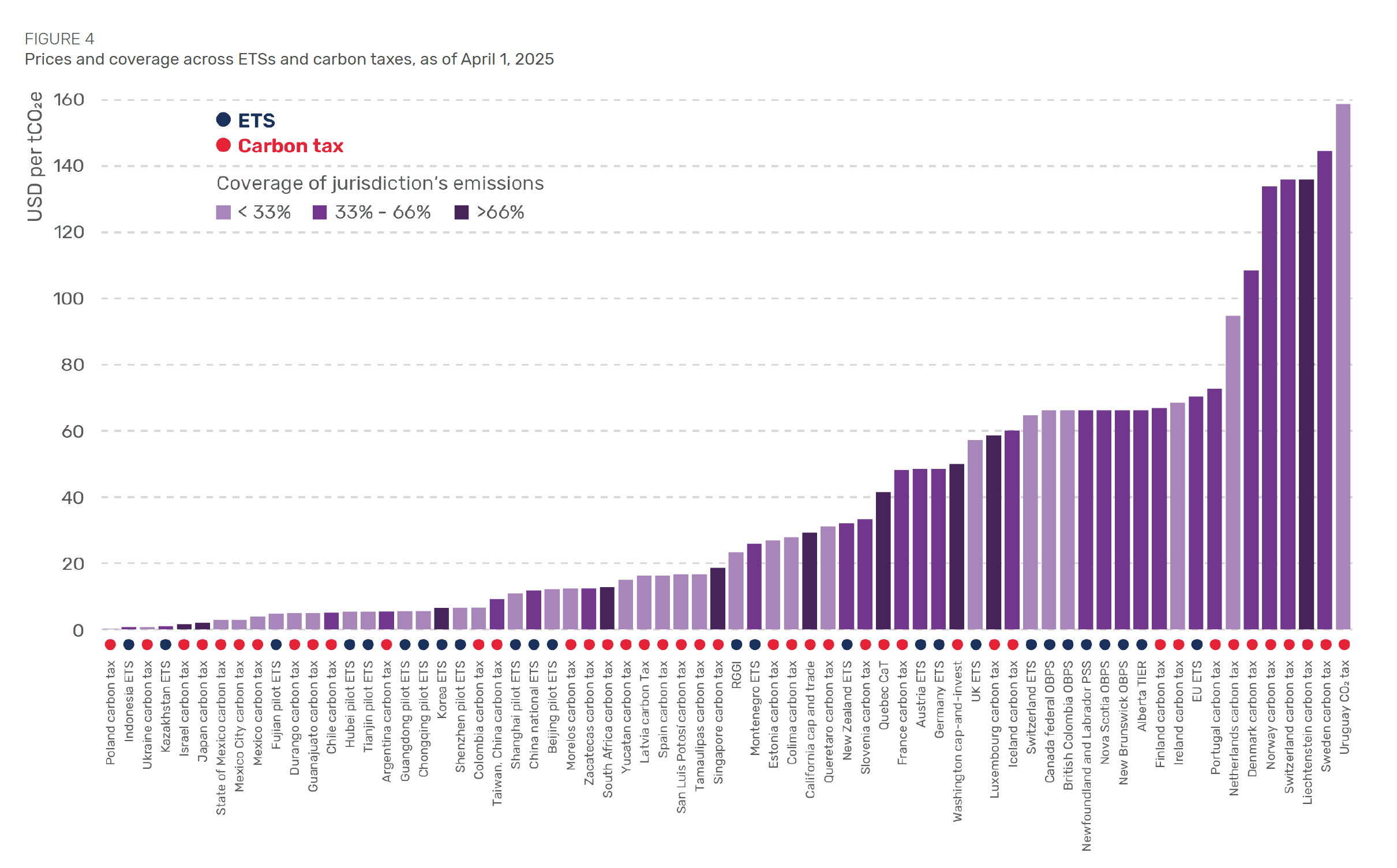

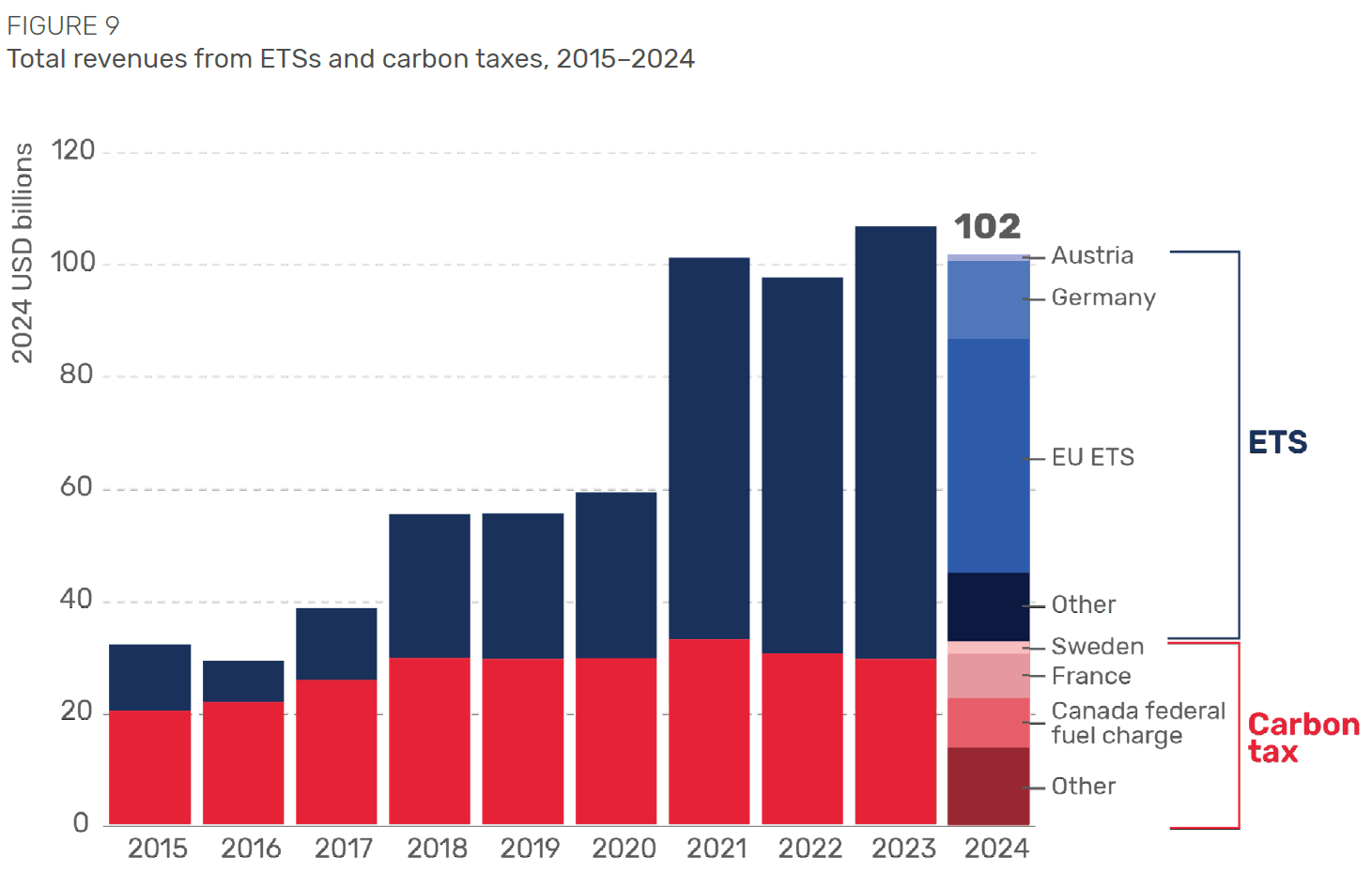

Main Carbon Markets

Stavins, R. (2019). The Future of U.S. Carbon Pricing (NBER working paper No. 25912)

Adding one important argument:

cap’n trade is under competition jurisdiction (technical, non qualified majority, not taken in account in tax burden) when taxes are under finance committees

easier to decide and vote